Evernorth, a cash management company backed by Ripple, Kraken, Pantera Capital and SBI Holdings, has a clear message to institutional investors: real banks are already using XRP. The company confirms that the next 18 months will not be about whether or not adoption news will happen, but rather about the scale of that adoption and the regulatory rules that will govern it.

The statement here is specific to numbers; Daily transactions on the XRP Ledger network have climbed to nearly 3 million transactions, up from around 1 million transactions in mid-2025. Names such as Bitstamp, Ripple’s RLUSD stablecoin, and Braza Bank stand out as the most active players on the network. This figure is real and documented, but its importance for the effectiveness of banking services remains subject to debate.

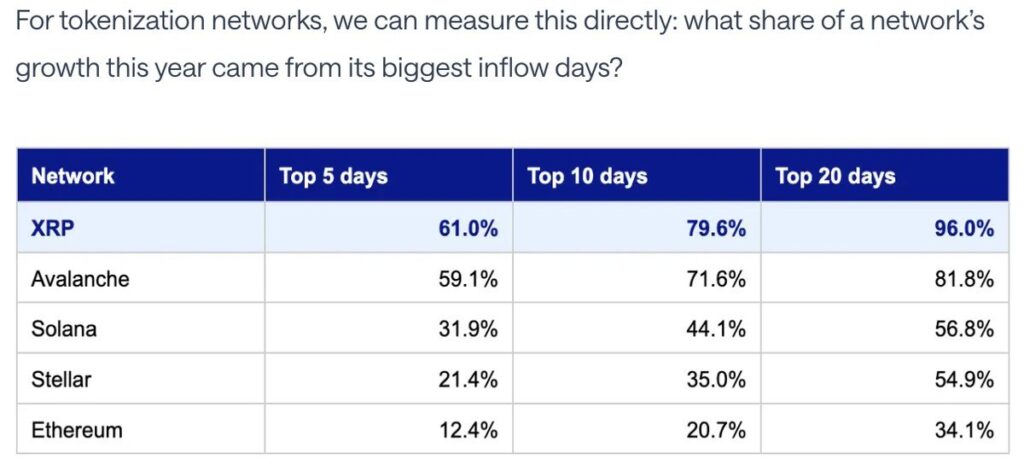

Structural tension is evident in the scene; According to reports, XRPL trading volume has tripled in approximately 12 months. At least one major European bank has also deployed its regulated, euro-denominated stablecoin on the XRP network, selecting it as one of four public blockchains for this purpose.

However, on-chain XRP data and exchange flows show a more complex story as to whether this volume represents sustainable banking infrastructure or simply a concentrated boom driven by a limited number of known players. Marketing talk and online data aren’t contradictory, they just don’t always say the same thing.

XRP News and Banking Leads: What Does the On-Chain Data Reveal?

See Ashesh BirlaCEO of Evernorth, said that the long-term value of XRP will come from banks and companies using it as working capital, not from individual transactions.

This proposal establishes a specific standard of proof: what matters is not speculative demand or exchange-traded fund (ETF) flows, but rather the volume of settlements issued by banks. Compared to this criterion, the data seem partly favorable and partly ambitious.

The increase in XRPL transactions to around 3 million per day is a documented fact, and the active names behind this movement, such as Bitstamp, RLUSD and Braza Bank, are specific financial institutions and not anonymous wallets or the result of fake transactions (Wash Trading).

In May 2026, Evernorth highlighted a token buyback of US Treasury bonds coordinated between Mastercard, JP Morgan’s Kinexys platform, Ondo Finance and Ripple, where the XRPL network was used as a common settlement layer. Ripple received funds in US dollars in Singapore outside of official banking hours.

Evernorth describes XRP as “settlement infrastructure for one of the largest inter-institutional blockchain transactions to date.” This incident actually happened and is not just an allegation.

But what the data has yet to confirm is whether these events represent a systemic and comprehensive adoption of the banking industry, or whether they are simply high-level first experiments.

Ripple’s on-demand liquidity (ODL) service has been operating since 2018, using XRP as an intermediary asset in cross-border corridors in markets such as the Middle East and Southeast Asia. The volumes in these corridors are real but they are geographically concentrated, not the “global banking corridor” that the headlines might suggest.

Although institutional transfers on XRPL will stabilize in 2026, Chainalysis data indicates increasing competition from USDC and wholesale central bank digital currency (CBDC) projects for share of institutional settlement flows.

The XRPL protocol is currently being developed to specifically address this gap; Pending changes include features like Token Escrow, an authorized DEX, and restricted environments. This compliance infrastructure is specifically designed to provide regulated organizations with reliable platforms and guaranteed settlement flows across the network.

The proposed XRP lending protocol (XLS-66) would integrate single-asset XRP vaults, term loans, and ZK-enhanced privacy directly into the network, eliminating the need for external smart contracts or software bridges. Auditors are currently voting on XLS-66, which requires a supermajority of 80% to activate.

This project has not yet been implemented. While analysts see this proposal as an opportunity to open up $100 billion in loans and collateral on XRPL, for now it is just paper infrastructure waiting to reach consensus, not actual banking activity on the network.

Banks Adopt XRP: Does the Data Reflect Market Ambitions? appeared first on Cryptonews Arabic.