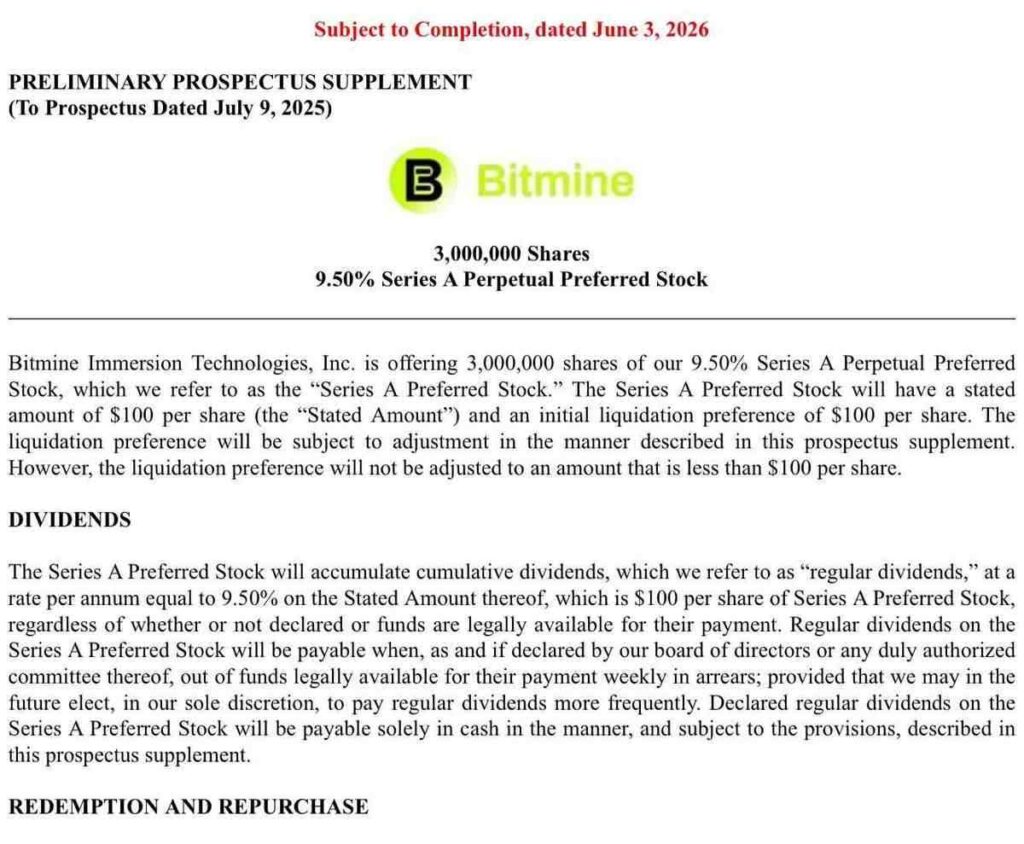

In today’s Ethereum news, BitMine Immersion Technologies filed with the U.S. Securities and Exchange Commission (SEC) on Wednesday to launch a Class A perpetual preferred stock offering, comprising 3 million shares at $100 per share, with a cumulative annual dividend of 9.5%. Proceeds from this offering were explicitly allocated to acquiring Ethereum, expanding ETH staking infrastructure, and investing in the network ecosystem.

This offering mirrors the structure pioneered by treasury giant Bitcoin Strategy, but includes a mechanism that Bitcoin cannot replicate: staking. The question the market is asking now is whether BitMine’s move is just a one-off capital raise or whether it is the start of a larger trend of mining companies moving from hashrate-based revenue to institutional ETH revenue as a sustainable business model.

Ethereum News: Mining Strategy vs. Staking Model: Why Does This Change Make Financial Sense?

The main argument for this change depends on the structure of the market; Bitcoin mining generates revenue through block rewards and transaction fees, but requires ongoing capital expenditures on hardware, power contracts, and cooling infrastructure. With each halving cycle, profit margins shrink significantly.

In contrast, Ethereum staking generates a return on balance sheet assets, currently between 3% and 5% per year, without incurring the same enormous operational expenses. BitMine’s preferred stock structure reinforces this logic; Strategy sold around 32 BTC earlier this year – its first sale since 2022 – to fund a dividend on its STRC preferred stock that yields 11.5%.

This sell-off briefly pushed Bitcoin below $62,000 and sparked caution in the market. BitMine’s counter-strategy demonstrates that a company with significant ETH reserves can fund its dividend obligations through staking proceeds rather than liquidating the underlying assets, which represents a fundamentally different capital structure.

BitMine President Thomas Li highlighted this point at the Proof of Talk conference in France, explaining that ETH digital asset vaults can use staking proceeds to fund grants to the Ethereum ecosystem, turning revenue generation into both a financial and governance engine. The company’s stated intention to expand its validation infrastructure through its MAVAN initiative indicates that this is real operational planning and not just media statements.

For his part, Jeffrey Kendrick, head of digital assets research at Standard Chartered Bank, sees this structural advantage – funding operations coming from staking proceeds versus forced coin sales – as a fundamental reason why ETH treasury companies can outperform their Bitcoin counterparts over time.

What optimists miss: stake returns are not constant and switching costs are real

The “yield as dividend source” argument is only valid if Ethereum staking returns remain stable enough to cover preferred stock obligations. The truth is that it is not fixed; The annual percentage yield (APY) of ETH fluctuates based on network participation rates, maximum mined value (MEV) requirements, and protocol-level changes.

A 9.5% premium dividend funded with a 3%-5% participation yield is not considered self-sustaining without additional ETH accumulation or additional revenue, which is exactly why BitMine’s press release mentions acquiring more ETH as a key payout goal.

Mining companies have also inherited operational structures that pure treasury companies do not have, such as restrictive covenants, physical infrastructure costs, and shareholder expectations based on mining economics, which do not disappear overnight. Moving from a mining strategy to a staking-based treasury is not just a balance sheet reclassification, it is a complete overhaul of the business model that carries implementation risks at every stage.

Concentration risks increase the complexity of the landscape; BitMine publicly aims to control approximately 5% of the total circulating supply of Ethereum. Analysts have warned that having a single institutional holder of this size becomes a key variable in ETH price dynamics, amplifying both accounting gains and losses.

Ultimately, the mining strategy argument and the cash flow argument are two different things; The first concerns operational efficiency, while the second concerns market structure. In a related context, the infrastructure of the Ethereum system is improving, making large-scale mortgage operations more feasible, but this does not eliminate the balance sheet risks resulting from maintaining a volatile and concentrated asset within a capital structure that relies on financial leverage.

The article BitMine launches $300 million bid to acquire Ethereum appeared first on Cryptonews Arabic.