Marathon Digital Holdings, the largest Bitcoin mining company in America, announced the sale of Bitcoin worth almost $1.5 billion, giving away approximately 20,880 BTC at an average price of almost $70,137 per coin. The company also announced that it would not purchase additional mining hardware, preferring to move towards artificial intelligence infrastructure.

When the report was released, MARA stock rose 0.24%, while BTC-USD fell 1.39%, giving a negative signal to companies’ Bitcoin cash flow models.

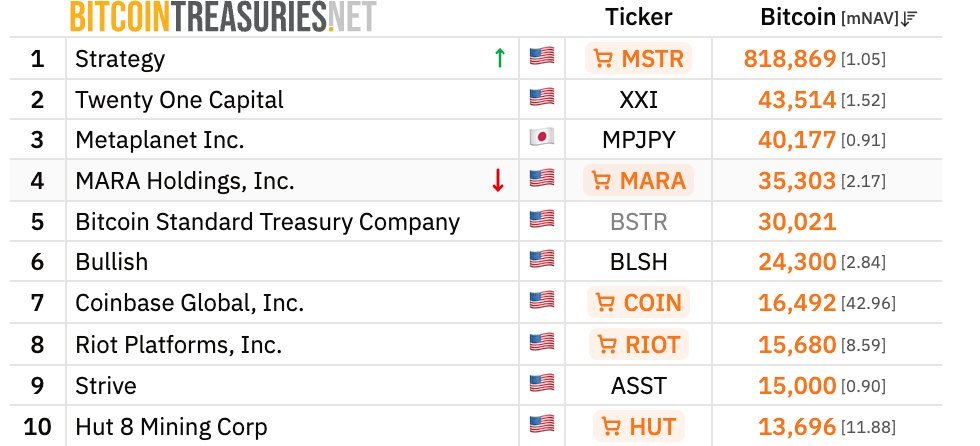

This sale reduced the company’s holdings from 38,689 BTC to approximately 35,303 BTC, placing it in fourth place among public companies holding Bitcoin.

Proceeds from the sale were used to repurchase convertible notes at a discount, reducing total debt from $3.3 billion to $2.3 billion, a decline of 30%, and generating an accounting gain of $71 million. Meanwhile, first-quarter revenue fell 18% year-on-year to $174.6 million, amid a net loss of $1.26 billion.

The Mechanics of Bitcoin’s $1.5 Billion Sale and Timing Implications

The sale reported by MARA represents approximately 54% of its previous Bitcoin stock and was carried out in phases including the sale of 15,133 BTC (worth $1.1 billion) between March 4 and 25, 2026.

At current market prices, the remaining 35,303 BTC are worth approximately $2.84 billion, which is still a significant reserve, but does not reflect the “cash first” strategy the company was promoting a year ago.

The importance of the details of the debt buyback is that the retirement of the discounted convertible bonds allowed MARA to record an accounting gain of $71 million, while eliminating the interest charges that made the Michael Saylor-inspired cash flow model increasingly fragile amid the halving of mining margins.

CEO Fred Thiel has not abandoned Bitcoin, but instead used it as liquidity to stabilize a balance sheet strained by $3.3 billion in convertible bonds.

This distinction is necessary; Selling Bitcoin to pay off debts is an operationally rational procedure under pressure on margins, and does not necessarily mean abandoning belief in the digital asset, and mixing the two leads to false analytical conclusions.

Do the selloffs reflect a decline in conviction or simply cash management?

There are two competing readings of this scene. A negative reading sees MARA issuing convertible bonds explicitly to mimic Michael Saylor’s strategy of accumulating Bitcoin, then reversing the trend and liquidating a significant portion of its assets in just two financial cycles.

According to this view, if the belief were real, the company would have found alternative debt servicing mechanisms instead of selling Bitcoin near cycle lows, making the move to AI merely a rebranding to cover up the failure of the cashflow model during stress testing.

Potential for $MARA the re-evaluation is massive if they decide to completely move to AI Data Center.

Fred Thiel @fgthiel said several notable things during his appearance on Bloomberg today about MARA Holdings and the broader Bitcoin/AI infrastructure market. Main points of… pic.twitter.com/fNwzRg6Pfs– Compounding Lab (@CompoundingLab) May 13, 2026

As for the operational results, they indicate that MARA produced 2,247 BTC in the first quarter, with the hash rate increasing by 33% year-over-year to 72.2 EH/s, meaning that it continues to mine strongly.

And spending $1.5 billion on AI infrastructure – supported by the acquisition of Long Ridge Energy’s 505-megawatt natural gas plant in Ohio for about $1.5 billion – is not a divestment of physical assets, but rather a rotation of capital from one physical infrastructure to another that offers better economic margins in the current interest rate environment.

Scott Melker, host of The Daily Wolf on Yahoo Finance, described the industry’s trajectory clearly: “Bitcoin miners are no longer just miners, they are AI companies that also mine Bitcoin. »

This change does not call into question the belief in Bitcoin, but rather a characterization of where capital returns lie. The Bitcoin Society’s recent cessation of purchasing Bitcoin for its treasuries reflects a similar dynamic, where companies’ conviction to hold BTC is tested on multiple balance sheets at once, not just at MARA.

The first conclusion is that the sale of MARA is primarily a debt management event involving a change in strategy. Even if the pressure on the Treasury model remains real, the story of a collapse in conviction seems exaggerated.

The article Marathon Digital Sells Bitcoin for $1.5 Billion, Moves to Artificial Intelligence appeared first on Cryptonews Arabic.